distribution¶

Available in: GBM, Deep Learning, XGBoost

Hyperparameter: yes

Description¶

Unlike in GLM, where users specify both a distribution family and a link for the loss function, in GBM, Deep Learning, and XGBoost, distributions and loss functions are tightly coupled. In these algorithms, a loss function is specified using the distribution parameter. When specifying the distribution, the loss function is automatically selected as well. For exponential families (such as Poisson, Gamma, and Tweedie), the canonical logarithmic link function is used.

By default, the loss function method performs AUTO distribution. In this case, the algorithm will guess the model type based on the response column type (specified using y). More specifically, if the response column type is numeric, AUTO defaults to “gaussian”; if categorical, AUTO defaults to bernoulli or multinomial depending on the number of response categories.

Certain cases can exist, however, in which the median starting value for this loss function can lead to poor results (for example, if the median is the lowest or highest value in a tree node). The distribution option allows you to specify a different method. Available methods include AUTO, bernoulli, multinomial, gaussian, poisson, gamma, laplace, quantile, huber, and tweedie.

If the distribution is

bernoulli, the response column must be 2-class categorical.If the distribution is

quasibinomial, the response column must be numeric and binary. (Available in GBM only.)If the distribution is

multinomial, the response column must be categorical.If the distribution is

gaussian, the response column must be numeric.If the distribution is

poisson, the response column must be numeric.If the distribution is

gamma, the response column must be numeric.If the distribution is

laplace, the response column must be numeric.If the distribution is

quantile, the response column must be numeric.If the distribution is

huber, the response column must be numeric.If the distribution is

modified_huber, the response column must be 2-class categorical.If the distribution is

tweedie, the response column must be numeric.If the distribution is

ordinal, the response column must be categorical with at least 3 levels.If the distribution is

custom, the response column must be numeric/binary/categorical depends on type of custom distribution.

NOTE: laplace, quantile, and huber are NOT available in XGBoost. custom is available ONLY in GBM.

The following general guidelines apply when selecting a distribution:

For Classification problems:

Bernoulli and Quasibinomial distributions are used for binary outcomes.

A Multinomial distribution can handle multiple discrete outcomes.

For Regression problems:

A Gaussian distribution is the function for continuous targets.

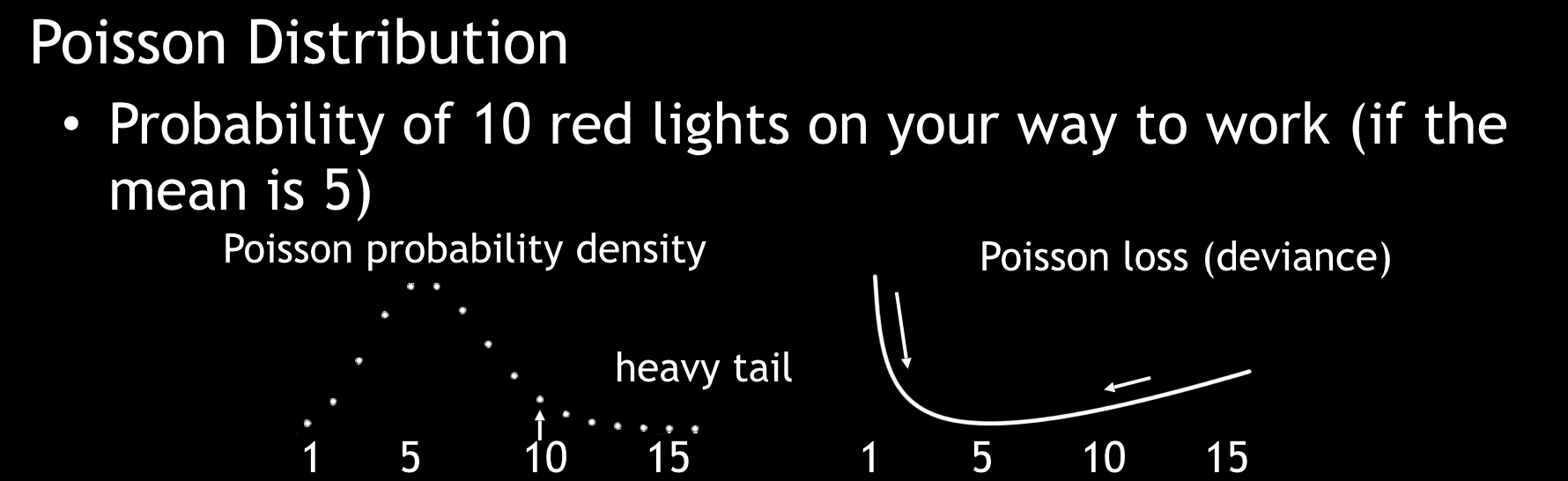

A Poisson distribution is used for estimating counts.

A Gamma distribution is used for estimating total values (such as claim payouts, rainfall, etc.).

A Tweedie distribution is used for estimating densities.

A Laplacian loss function (absolute L1-loss function) can predict the median percentile.

A Quantile regression loss function can predict a specified percentile.

A Huber loss function, a combination of squared error and absolute error, is more robust to outliers than L2 squared-loss function.

When quasibinomial is specified, the response must be numeric and binary. The response must also have a low value of 0 (negative class). Note that this option is available in GBM only.

When tweedie is specified, users must also specify a tweedie_power value. Users can tune over this option with values > 1.0 and < 2.0. More information is available here.

When quantile is specified, then users can also specify a quantile_alpha value, which defines the desired quantile when performing quantile regression. For example, if you want to predict the 80th percentile of a column’s value, then you can specify quantile_alpha=0.8. The quantile_alpha value defaults to 0.5 (i.e., the median value, and essentially the same as specifying distribution=laplace). Note that this option is not available in XGBoost.

When huber is specified, then users can also specify a huber_alpha value. This indicates the top percentile of error that should be considered as outliers. Note that this option is not available in XGBoost.

When custom is specified, then users must also specify a custom_distribution_func value. This is reference to loaded custom distribution function. For information how to load custom distribution see custom_distribution_func. If custom distribution is set, no deviance metrics (training deviance, validation deviance and mean deviance) are calculated.

For all distributions except multinomial and custom, you can specify an offset_column. Offsets are per-row “bias values” that are used during model training. For Gaussian distributions, they can be seen as simple corrections to the response (y) column. Instead of learning to predict the response (y-row), the model learns to predict the (row) offset of the response column. For other distributions, the offset corrections are applied in the linearized space before applying the inverse link function to get the actual response values. For more information, refer to the following link.

Some examples of response distributions are provided below.

Gaussian Distribution

Poisson Distribution

Laplace Distribution

Bernoulli Distribution

Equations¶

Where:

\(y\) is a true response

\(f\) is a predicted response

\(w\) is weight

Distribution Type |

Equation |

|---|---|

Bernoulli |

\(-2\times w\times(y\times\log(f))+(1-y)\times\log(1-f))\) |

Quasibinomial |

\(f= \begin{cases} -2\times w\times y\times\log(f) & \text{for } f>1 \\ -2\times w\times(1-y)\times\log(1-f) & \text{for } f<0 \\ 0 & \text{for } f=y \\ -2\times w\times (y \times\log(f)+(1-y)\times\log(1-f)) & \text{otherwise} \\\end{cases}\) |

Gaussian |

|

Poisson |

|

Gamma |

|

Laplace |

\(w \text{ }\times\mid{y-f}\mid\) |

Quantile |

\(f= \begin{cases}w\times QuantileAlpha \times(y-f) & \text{for }y>f \\ w\times(1-QuantileAlpha)\times(f-y)& \text{for } y \leq f \\\end{cases}\) |

Huber |

\(f= \begin{cases} w\times(y-f)^2 & \text{for } \mid{y-f}\mid \leq HuberDelta & \text{(Equivalent to wMSE)} \\ 2\times w\times(\mid{y-f}\mid -HuberDelta)\times HuberDelta & \text{for } y \leq f & \text{(Equivalent to wMAE)} \\\end{cases}\) |

Modified_Huber |

\(\text{With } z=(2\times y-1)\times f \\ f= \begin{cases}-4\times w\times z & \text{for } z\leq 1 \\ 0 & \text{for } z>1 \\ w\times z^2 & \text{otherwise} \\\end{cases}\) |

Tweedie |

with \(f=\text{link}(f)\), requires \(1>\text{Tweedie_Power}<2\): \(2\times w\times y^{(2-\text{Tweedie_Power})/((1-\text{Tweedie_Power})\times(2- \text{Tweedie_Power}))}-y \times \exp(f\times(1-\text{Tweedie_Power}))/ (1-\text {Tweedie_Power})+ \exp(f\times(2-\text{Tweedie_Power}))/(2-\text{Tweedie_Power})\) |

Link/Inverse Link Functions |

Equation |

|---|---|

Identity: Gaussian Huber, Laplace, Quantile |

|

Log: Multinomial, Poisson, Gamma, Tweedie |

|

Logit: Bernoulli, Quasibinomial, Modified_Huber |

|

Inversion |

\(link(f)= linkInversion(f) = \begin{cases}min(-1e-5, f) & \text{for }f<0 \\ max(-1e-5, f)& \text{for }f>0 \\\end{cases}\) |

Ologit |

|

Ologlog |

|

Oprobit |

|

Note: Inversion, Ologit, Ologlog, and Oprobit are not associated with concrete distributions but can be used with a custom distribution.

Example¶

library(h2o)

h2o.init()

# import the cars dataset:

# this dataset is used to classify whether or not a car is economical based on

# the car's displacement, power, weight, and acceleration, and the year it was made

cars <- h2o.importFile("https://s3.amazonaws.com/h2o-public-test-data/smalldata/junit/cars_20mpg.csv")

# set the predictor names and the response column name

predictors <- c("displacement","power", "weight", "acceleration", "year")

response <- "cylinders"

# split into train and validation sets

cars_splits <- h2o.splitFrame(data = cars, ratios = 0.8, seed = 1234)

train <- cars_splits[[1]]

valid <- cars_splits[[2]]

# try using the distribution parameter:

# train a GBM

car_gbm <- h2o.gbm(x = predictors, y = response, training_frame = train,

validation_frame = valid,

distribution = "poisson",

seed = 1234)

# print the MSE for your validation data

print(h2o.mse(car_gbm, valid = TRUE))

import h2o

from h2o.estimators.gbm import H2OGradientBoostingEstimator

h2o.init()

# import the cars dataset:

# this dataset is used to classify whether or not a car is economical based on

# the car's displacement, power, weight, and acceleration, and the year it was made

cars = h2o.import_file("https://s3.amazonaws.com/h2o-public-test-data/smalldata/junit/cars_20mpg.csv")

# set the predictor names and the response column name

predictors = ["displacement","power","weight","acceleration","year"]

response = "cylinders"

# split into train and validation sets

train, valid = cars.split_frame(ratios = [.8], seed = 1234)

# try using the distribution parameter:

# Initialize and train a GBM

cars_gbm = H2OGradientBoostingEstimator(distribution = "poisson", seed = 1234)

cars_gbm.train(x = predictors, y = response, training_frame = train, validation_frame = valid)

# print the MSE for the validation data

cars_gbm.mse(valid=True)